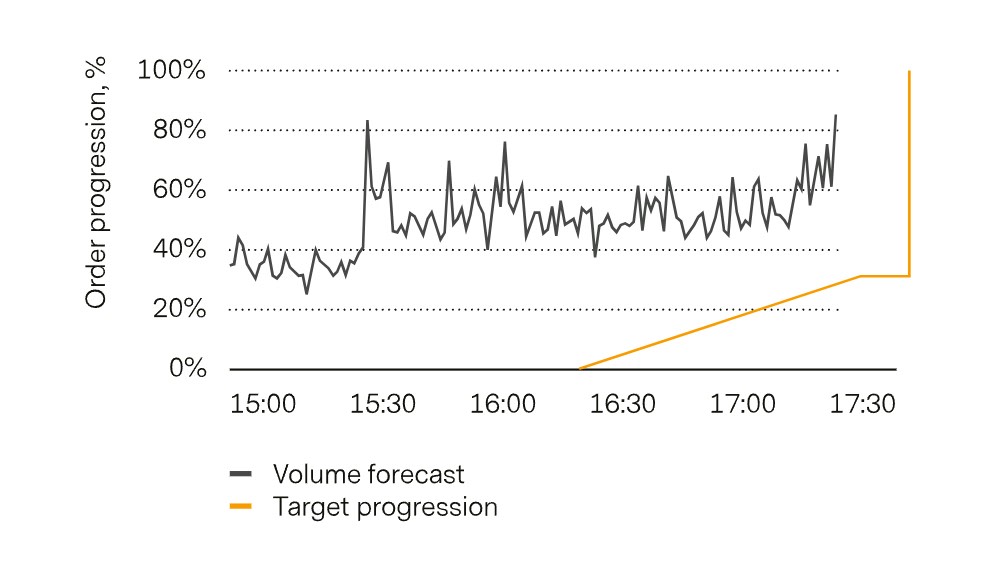

Large portfolio trades that are benchmarked at the closing price require special care. Our Target Market-on-Close algorithm automatically assesses expected liquidity and minimizes the potential market impact at the closing auction for large orders.

The client flow that our algorithms handle on a daily basis varies in nature and profile. The two most frequently used algorithms in our portfolio are the VWAP, which targets the volume-weighted benchmark price, and PACE, our flagship algorithm that combines implementation shortfall and liquidity-seeking styles and is benchmarked at arrival price. The use cases for these algorithms range from very brief aggressive trades to multi-day slow executions on some illiquid instruments.

However, in many cases, clients’ needs necessitate sending an order specifically to the closing auction. This occurs with individual stocks when traders anticipate a substantial overnight gap, for example, due to an upcoming earnings call the next morning. It is even more common for program trades when a portfolio manager rebalances a portfolio that is benchmarked at the closing price. In these situations, the use of traditional algorithms, such as VWAP, carries market risk—the difference between the benchmark and the closing price.

For such program trades, traders often send “at-the-close” market (rarely limit) orders that simply enter the closing auction. This type of trade, however, places an extra burden on the traders themselves: they must ensure that their order is not so large that it pushes the price of the auction or, in the worst case, leads to a “non-opening,” when the auction book cannot uncross due to imbalance. For a few instruments it is a relatively straightforward task to compare order size with expected auction volume. However, for a portfolio of 30 to 50 stocks, it becomes burdensome. Further difficulty arises when the trade is large for some of the instruments, requiring the trader to plan the execution to start during the day and select an appropriate algorithm.

Show more articles

Show more articles