Vontobel's SOR Infrastructure

Today, the European exchange landscape is fragmented more than ever. MiFID II, post-Brexit, and the nonequivalence of the Swiss exchanges are some of the factors behind this. As a response to this new situation, we have developed our own smart order router (SOR) over the last three years, which clearly positions us at the top of the Swiss market and puts us on the same level as global brokers and Tier-1 banks in Europe.

01010011 01001111 01010010 – this binary ASCII code represents the word “SOR” in the digitized world. Although the ASCII code standard is now more than 50 years old, it is still successfully used in our IT systems. In the Trading Product Development department, we connect the real world with the digital one, leveraging available tools and systems, or building them ourselves if it is economically justified. In order for us to successfully develop systems in the trading domain, we need to understand how the real world can be mapped onto the digital one. Therefore, we require specialists such as software engineers, quants, and IT solution architects who are able to transform analog business procedures into formalized digital processes.

When I talk with the traders from the Electronic Sales Trading team, they often joke that I am able to process data in this type of binary form in my brain. I can assure you that this is not the case. However, today it is almost impossible to work in an industry that digitalization has not yet disrupted. In cash equities, electronic trading was introduced more than 25 years ago. Since the start, the systems involved have been continuously improved, refined, and adapted to ever-changing conditions. In this article, you can read more about what we have done over the past few years to stay on the cutting edge of the electronic trading space. 01000111 01001100 01001000 01000110.

Creating a magic moment

When you look back on your career, you will remember the best boss you had, the best team you were on, and the best project you worked on. All of those memories will change over time as you make new memories. The more you experience, the more you will have to compare these memories to.

I wanted the project to build our own SOR infrastructure to serve as all of these things for everyone who worked on the project. If I was only able to form the best team that any of the participants had worked on, then that would have been a great success. I can only speak for myself, but for me, it has been one of the best projects I have worked on and definitely the best team I have been a part of!

The story starts in autumn 2019. At that time, we had been using SOR solutions. All of them came with pros and cons. With our latest software license, the biggest con was an inflexible software improvement process, which came with a very special piece of software that is only licensed by a handful of clients. We lacked the flexibility we needed to react to all of our clients’ wishes. In addition, the product had come to the end of its life span, and we were looking at alternatives.

In addition to a replacement, one alternative we looked into was the decision to make our own. We carefully considered this option and then drew up a promising business plan that covered all of the details, including charts that pointed to the first quadrant in terms of cost and performance.

In the end, the decision to make or buy came down to a proof of concept that showed us that we have the right tech and experience to do this in-house. With the amazing engineers from our team, including Tobias Moser, Cyril Hottinger, Evangelos Papakonstantis, and everyone else who was involved in the project, we could see a PoC working in just a few weeks. With design patterns like the finite-state machine (FSM) and the actor programming model implemented by the Akka framework, we were able to use the right abstraction layers to build our version of an SOR infrastructure on top of this foundation.

Once we had the proof of concept, we had everything we needed to carry out a realistic estimation, and, together with the business plan, we pitched our senior management on the “make” option. They accepted our pitch in January 2020, and so we had to deliver.

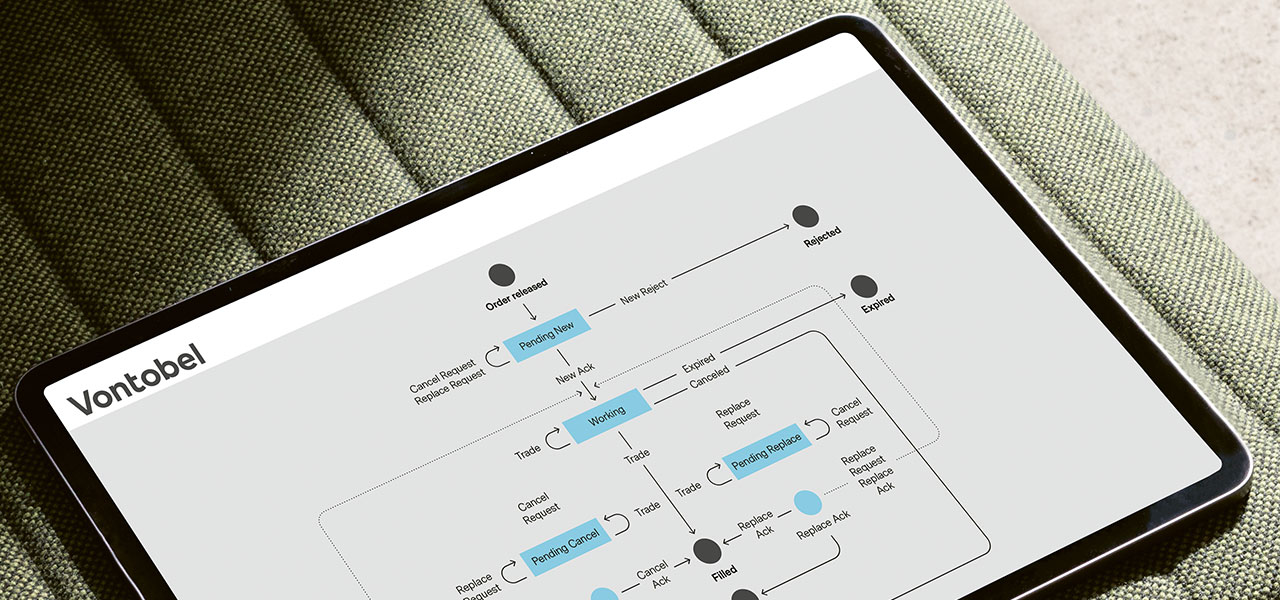

Chart 1: Life-Cycle-Management of a PULS child order

After 15 months of very hard work, many releases, hundreds of unit tests, endless sleepless nights, and plenty of blood, sweat, and tears, the SOR went live and operational. We needed a name for it, and an internal team poll found it. Our new SOR is called PULS because it functions at the heart of our equity execution management system. By May 2021, all of the existing SOR profiles – these are strategies for how to trade on the markets – had been built. Even better, all the profiles we always wanted to build, but were unable to due to a lack of flexibility, had been built as well. This means we went live not with a product that merely replaced the existing one, but with an even better version of what we had before.

But the story does not end there. Since May 2021, we have taken the opportunity to build even more on top of the PULS infrastructure, which turned out to be the next-level framework we always wanted to have. In the past year, we have created special profiles to not only trade equities but also structured products, ETFs, and fixed-income products on European cash equity markets.

Looking back now on the whole initiative, I can say that we created more than just one magic moment – we created many of them. For me, the most important aspect is the fact that our team has been able to build and maintain higher-quality cutting-edge technology than an existing software provider. It is fair to say that it has been easier to build software that fits 100 percent of our specific requirements than it is to build a full-fledged software product that can be adopted by many clients who all have different requirements.

The best thing about our new situation – now that PULS is live – is that we now have a tool that meets all of our needs, its intellectual property belongs to Vontobel, and we have it under our full control. We can decide what will be the next improvement or the next bug fix. We are now in the driver’s seat of our SOR infrastructure.

Why did we build our own SOR infrastructure?

The smart order router is the piece of software that makes the final decision on which market is best to trade on at what time. On European cash equity markets, this corresponds to the heart of the execution platform. Vontobel has licensed various smart order router software in the past, but has never been fully satisfied with the results. For this reason, at some point, we reached the point where we made the decision to bring our smart order router infrastructure under our full control. This means we developed the software by ourselves in the Trading Product Development department, and we built up a corresponding IT architecture to operate the SOR.

One of the main reasons for us to build our own infrastructure was all of the small details that we were unable to control in the software products that we had licensed, either because the software did not support it, the concept did not fit, or it simply did not work anymore because the market conditions had changed. One concrete example is the dynamic adjustment of network latencies. The network topology can change at any time – for example, an excavator can cut a fiber optic cable that we use to send our messages from our data center to another one at any moment. If you think this is an improbable example, you might be wrong. It can occur a few times a year. With the existing product, latency adjustment was only possible with millisecond precision, which is no longer sufficient in reality. Nowadays, we have to be able to scale down to microseconds. Today, we are able to react in such a scenario down to the microsecond level. Our SOR is able to add the least necessary artificial delay to the child order, so that all the child orders arrive simultaneously at marketplaces where we want to trade in parallel.

To demonstrate the best execution to our clients, we have created a database to store every event created in the decision tree of the lifecycle of the full trading process. With our Trading Analytics Platform™, we measure the SOR KPIs and continue to improve prices and fees where we can.

Did we use AI, blockchain, or polyglot cloud infrastructure to build PULS?

The simple answer is no. We used plain old Java technology coupled with the Linux operating system. Everything ran on purely physical, nonvirtualized hardware, which are referred to as bare-metal servers. The software design concepts on which we were building, like the finite-state machine or the Actor programming model, are from the 1970s or even older. We see these concepts as universal, and they have proven to be bulletproof software concepts in recent decades.

Published on 18.09.2023 CEST

ABOUT THE AUTHORS

Show more articles

Show more articlesRoman Würsch

Head Trading Platform Development

Roman Würsch heads the Trading Platform Development department in the Transaction Banking unit at Vontobel. He is responsible for the development, operations, and strategic direction of the cross-asset execution platform, serving both internal and external clients.